AI-DrivenPersonalisationinFinancialRecommendations

If I had to sum it up in one line: UK firms now get better results from a hybrid model - AI for timing and relevance, rules for control and compliance.

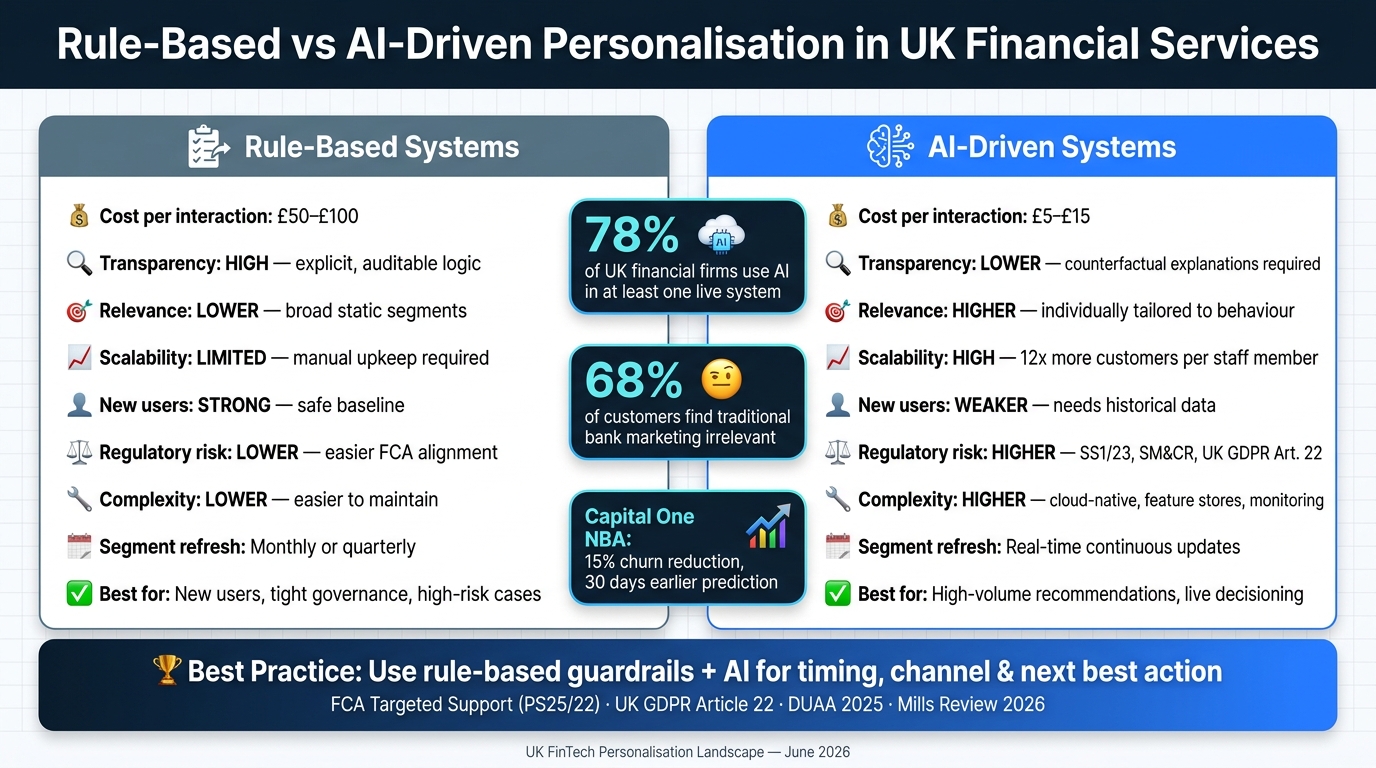

I can see the split quite clearly in the data. On one side, 78% of UK financial services firms now use AI in at least one live system. On the other, rule-based setups still matter because they are easier to audit and keep within FCA expectations. That matters when 68% of customers say old bank marketing feels irrelevant, and when support rules now demand tighter customer grouping under the FCA’s Targeted Support update from March 2026.

If you want the short version, here it is:

- Rule-based systems are easier to check, easier to govern, and often safer for high-risk use cases.

- AI-driven systems are better at spotting intent, reacting to behaviour, and sending the right prompt at the right time.

- Rules often lag because segments may only update monthly or quarterly.

- AI can cut cost from about £50–£100 per manual support interaction to around £5–£15 in automated models.

- AI also brings more risk around bias, explainability, and customer challenge rights under UK GDPR Article 22 and the DUAA 2025.

- New users are still a weak spot for AI because there is less history to work from.

- The best fit for many UK FinTech teams is AI plus rule-based guardrails, not one or the other on its own.

Rule-Based vs AI-Driven Personalisation in UK Financial Services

Quick Comparison

| Area | Rule-based | AI-driven |

|---|---|---|

| How it works | Fixed if-then logic | Model-led scoring and live signals |

| Main strength | Clear control and audit trail | Better relevance and timing |

| Main weakness | Static segments go out of date | Harder to explain and monitor |

| Best for | New users, tight governance, high-risk cases | High-volume recommendations, live decisioning |

| Scale | Limited by manual upkeep | Handles much larger volumes |

| Cost per interaction | £50–£100 | £5–£15 |

| Compliance view | Lower model risk | More checks needed for review, challenge, and bias controls |

So when I look at this space in June 2026, the answer is not “rules or AI”. It is simpler than that: use rules to set the limits, and use AI inside those limits where it adds better judgement on timing, channel, and next action.

sbb-itb-1051aa0

1. Rule-Based Personalisation

Rule-based personalisation is still common because it’s easy to control. The logic is plain to see, which makes sign-off and oversight simpler. But there’s a catch: once customer behaviour starts shifting, these systems often lag behind. They rely on fixed if-then rules tied to set customer attributes and RFM signals.

Segmentation Accuracy

The main weakness is straightforward. These systems group customers by profile, not intent. So two people with the same demographics can end up seeing the same offer, even if they want very different things.

There’s also a timing problem. Segments are often updated monthly or quarterly, which means a high-net-worth customer showing signs of churn may not be picked up until the next batch run. When the segment is old, the offer is old too.

Responsiveness and Scalability

Rule-based engines don’t learn after launch. If the market changes, someone has to step in and adjust the rules by hand. That can work at small scale, but it gets messy fast.

As product lines grow, many teams hit a ceiling of around 4–8 segments per product area before upkeep starts costing more than the gain. And the cost gap can be sharp: manual processes in financial support often run at £50–£100 per interaction, compared with £5–£15 for automated AI-driven models.

Explainability and Bias Controls

This is where rule-based systems still hold their ground. They’re the easiest to audit because the logic is explicit, and protected characteristics can be left out of the rules.

That level of visibility helps explain why rule-based logic still sits inside many compliance workflows. You can trace the decision path without much guesswork.

Compliance and Operational Risk

The FCA’s Targeted Support framework (PS25/22) says segments must be granular enough to make sure the support is suitable for every person inside them. That puts rule-based systems in a tough spot. They need to stay precise, but not become so complex that they’re hard to run.

Data silos make things worse. Outreach gets split across channels, so a customer might receive an offer in one place after already taking the same product somewhere else. At that point, the recommendation starts to look out of touch.

That’s the limit AI-driven segmentation is built to overcome.

2. AI-Driven Segmentation and Recommendation Engines

AI systems deal with the delay built into fixed segments by updating customer profiles all the time. Instead of relying on static cohorts, these engines build a live profile from transactions, behaviour, portfolio changes and life events. The result is segmentation at the individual level, not broad buckets that go stale.

Segmentation Accuracy

Rather than sorting people into fixed demographic groups, AI groups customers by behaviour, goals and signals of change. It blends stated goals and risk questionnaires with app usage and market-response signals. That matters because personalisation now rests on the next action, not just the next product.

This is the shift from Next Best Offer to Next Best Action (NBA). The system works out the right action, channel and timing - such as a proactive savings prompt or a portfolio drift alert - instead of simply pushing a product.

Responsiveness and Scalability

Speed is where AI systems stand out most. They use batch and real-time inference to deliver recommendations within tight latency budgets. That speed matters because financial signals can lose their value fast.

Capital One's "Next Best Action" engine analyses over 1,000 variables per customer, predicts churn risks up to 30 days earlier than manual methods and delivers a 15% reduction in churn. At scale, the cost case is hard to ignore: AI-driven models can handle 12 times more customers per staff member than manual processes.

Explainability and Bias Controls

Better relevance only works if people can still understand the logic and challenge it. That's the hard bit.

Use SHAP for driver analysis, but pair it with plain-language counterfactual explanations and continuous bias monitoring. The FCA and PRA expect explanations customers can understand and question - for example: "If your credit utilisation were below 30%, you would be approved."

Compliance and Operational Risk

Once recommendations start shaping financial outcomes, explainability stops being a nice-to-have and becomes a compliance issue. Finer segmentation can improve targeting, but it also increases the risk of unfair outcomes when oversight is weak.

Bank of America's AI assistant, Erica, uses sentiment analysis to adjust its messaging tone based on how a customer is interacting, leading to a 35% increase in engagement. But this kind of adaptive messaging needs active supervision. It should stay within clear governance boundaries, not run on autopilot.

Under UK GDPR Article 22 and the Data Use and Access Act (DUAA) 2025, firms must provide human review so customers can challenge automated decisions. The Section 103 right to complain, which commenced on 19 June 2026, gives consumers a direct route to challenge automated decision-making in financial services. The FCA's Mills Review, launched in January 2026, is examining whether Consumer Duty needs specific revisions as AI develops through 2030.

Pros and Cons

The trade-off comes down to control versus adaptation.

The table below shows where each approach does well and where it falls short.

| Feature | Rule-Based Systems | AI-Driven Systems |

|---|---|---|

| Transparency | High; logic is explicit and auditable | Lower; regulators increasingly expect counterfactual explanations rather than technical model metrics |

| Relevance | Lower; relies on broad, static segments | Higher; individually tailored to behaviour |

| Scalability | Limited; manual effort grows with volume | High; scales to large user bases at low marginal cost |

| Works for New Users | Strong; works as a safe baseline for new users | Weaker; needs historical data to be effective |

| Regulatory Risk | Lower; easier to align with FCA targeted support | Higher; requires SS1/23, SM&CR and UK GDPR Article 22 safeguards |

| Implementation Complexity | Lower; easier to maintain and audit | Higher; requires cloud-native architecture, feature stores and monitoring |

| Operational Cost per Interaction | £50–£100 | £5–£15 |

Rule-based systems make sense when data is thin, the customer is new, or governance needs to stay tight. They give teams a safer starting point and make it easier to trace why a decision was made.

AI-driven systems flip that balance. They offer more relevant outputs and can handle speed and scale far better, but they come with added governance work. Model drift, biased outputs, and the need for continuous monitoring are not edge cases; they are part of day-to-day operations.

In regulated finance, that point matters. A recommendation has to fit the customer in front of you, not just people who look similar in the data. That’s why compliance and AI need to be built together from the start, not added as an afterthought.

These trade-offs shape when rules make more sense, when AI is the better fit, and when a combined approach is the smarter call.

Conclusion

Neither approach wins across the board. Rule-based personalisation fits tightly controlled, high-risk cases. AI-driven segmentation fits high-volume, real-time recommendations. In practice, that leads to a hybrid operating model.

The workable answer is hybrid. AI adds context to suitability; it doesn’t replace it. The strongest UK implementations use AI for predictive power and better timing, then use rule-based guardrails to keep outputs compliant and explainable.

For UK FinTech teams, the path is pretty clear: start with rules for suitability, add AI for relevance, and build compliance in from day one.

FAQs

When should a firm use AI instead of rules?

A firm should shift from static, rules-based methods to AI when scale, accuracy, or personal relevance starts to outgrow what manual work can handle.

Rules are fine for simple, steady workflows. But they tend to miss messy details and changes in customer behaviour. AI makes more sense when a firm needs to analyse large, multi-dimensional data sets and turn that into personalised, real-time action.

How can AI recommendations stay compliant in the UK?

In the UK, AI-led financial recommendations stay compliant when firms build regulation into the system from day one. The FCA doesn’t have AI-only rules, so businesses need to work within the rules that already exist, above all Consumer Duty and the advice–guidance boundary.

That means putting proper governance in place, using validated segments, setting clear limits on what the service does, and making decision logic easy to follow. It also means keeping human oversight in the loop and having a lawful basis under UK GDPR. Where automated decisions are used, firms need to document them and explain them clearly in their privacy notices.

What is the best way to handle new customers with little data?

When a new customer arrives, there often isn’t much data to work with. That makes standard collaborative filtering less useful, because it leans on past interactions.

A better way to handle this cold-start problem is to use content-based filtering as a safety net.

Instead of waiting for behaviour data to build up, it uses structured product metadata, such as risk tiers, fee structures, liquidity windows, and regulatory classifications, to position products in a sensible way from day one.

Then, as the customer starts to engage, behavioural signals and contextual augmentation can sharpen and refine the recommendations.

Lets grow your business together

At Antler Digital, we believe that collaboration and communication are the keys to a successful partnership. Our small, dedicated team is passionate about designing and building web applications that exceed our clients' expectations. We take pride in our ability to create modern, scalable solutions that help businesses of all sizes achieve their digital goals.

If you're looking for a partner who will work closely with you to develop a customized web application that meets your unique needs, look no further. From handling the project directly, to fitting in with an existing team, we're here to help.